Advice forPolicy Holders

We understand that making an insurance claim is not something you planned for and that the experience may involve processes, people and terminology that are unfamiliar to you. Below, we explain the claim process, the role a loss adjuster plays in that process, and how you can appoint a loss adjuster to work on your behalf.

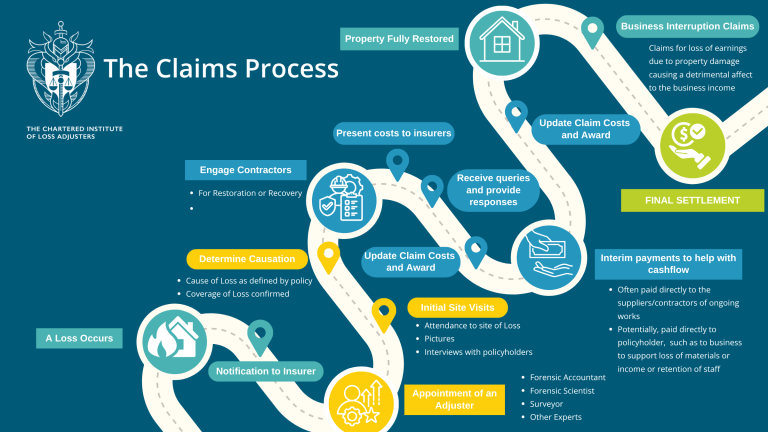

How a claim works

What is a loss adjuster?

A loss adjuster is an impartial evaluator who specialises in the handling and resolution of insurance claims.

In some cases, the loss adjuster will be employed by the insurer and report directly back to them. Most insurance companies will have a panel of loss adjusters or loss adjusting firms to take care of any claims. Some larger insurance companies have their own in-house loss adjusting teams instead.

However, you as the policyholder can also appoint one to work on your behalf. Either way, a loss adjuster will ensure that your interests are protected and negotiate with the insurance company for a fair outcome.

Loss adjusters are often the ‘second responder’ to a claim or incident. This often means that, after the police, ambulance or firefighters have left the scene, the next arrival will often be a loss adjuster.

The job of a loss adjuster is to use reports alongside their accumulated knowledge and experience to assess the damage (such as damage to property or disruption to earnings), identify the cause and check policies to verify that:

- The right insurance is in place to cover the loss

- All conditions of the insurance policy have been met

- The amount being claimed matches the actual costs of repairs or replacements

A loss adjuster will also be able to recommend the best way for the affected individual or company to get back on their feet.

Why should I appoint a Chartered loss adjuster?

When appointing a loss adjuster to work on your behalf, you may come across professionals who refer to themselves as claim preparers, claim managers, loss assessors, or similar. However, it is strongly recommended that you appoint a Chartered Loss Adjuster.

A Chartered Loss Adjuster is a qualified member of the Chartered Institute of Loss Adjusters (CILA) and will use the post-nominals ACILA or FCILA. They have passed rigorous examinations, demonstrated professional competence, and must adhere to a strict code of conduct. This gives you confidence that they will act with integrity, independence, and technical expertise.

Should you have a concern about the conduct of any claims professional, you should first raise this with their employer or, where applicable, the insurer. If your claim has concluded and you believe that a CILA member acted inappropriately, you may submit a complaint to us by following the instructions outlined at the bottom of this page.

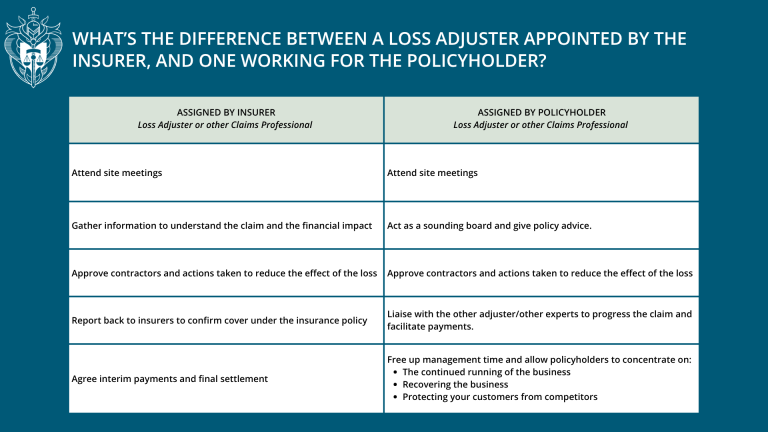

What’s the difference between a loss adjuster appointed by the insurer, and one working for the policyholder?

What happens after the insurer is notified of the loss?

In the first instance, a loss adjuster will ask lots of questions. This enables them to get a good understanding of your circumstances and the claim you wish to make. If your claim involves the need for emergency action, such as arranging alternative accommodation, the loss adjuster will provide advice on this. You can appoint your own adjuster at any time, but it is better to have a representative as soon as possible to support you during the initial stages of the claim.

A loss adjuster will typically arrange to meet with you and your representative in person and, if your claim involves damage to property, this meeting may include an inspection of your property. In advance of their visit, the loss adjuster will typically ask you to have ready any information or documentation that supports your claim.

Having gained a good understanding of your claim, the insurer’s loss adjuster will then check your insurance policy to establish whether your claim is covered. This may involve communication with your insurance company, insurance broker and/or other experts.

If you have appointed your own adjuster, following this initial meeting you will work together to obtain information to support your claim, and present this to your insurers.

Who pays for the loss adjuster?

If your insurance company has appointed a loss adjuster to handle your claim, your insurance company will pay that loss adjuster’s fee.

If you have appointed a loss adjuster to work on your behalf, you will pay that loss adjuster’s fee.

Some insurance policies include cover for such fees under a “Claims Preparation Clause”. You can also purchase insurance to cover the cost of loss adjuster fees in the event of a claim, so you may wish to check your insurance policies and/or speak to your insurance broker to find out whether you have purchased this type of insurance.

Questions

If you have any questions about the information outlined this process, please do not hesitate to contact the team at info@cila.co.uk for more help.

Making a complaint

While we hope that your experience with loss adjusters is always positive, we understand that this may not always be the case. If you wish to complain to the Institute about a loss adjuster, the following criteria must be met:

• The complaint must be regarding a loss adjuster who is a member of the CILA

Contact info@cila.co.uk to verify membership status.

• The complaint must relate to behavior or actions that break our Guide to Professional Conduct

CILA is a membership body not a trade body. This means that, while we can investigate breaches of behavior or actions by a member, we do not hold authority over companies or claims outcomes.

If your case matches the above conditions you can proceed with making a complaint. Please read this document to find out how.